Tax law requires individuals who have reached age 72 to begin taking minimum distributions from their traditional IRA accounts. These are referred to as a required minimum distribution or RMD. The RMD amount is the value of the IRA account on the last day of the prior year divided by the distribution period from the Uniform Lifetime Table, corresponding to the taxpayer’s attained age. For example, if an individual had their 75th birthday in the current year, the distribution period from the table is 24.6. If the balance in the IRA was $500,000 on the last day of the prior year, then the individual’s RMD for the current year would be $20,325 ($500,000/24.6). (The IRS develops the Table using mortality rate data and updated it effective with 2022 distributions.)

Qualified Charitable Distributions – The tax law also permits individuals aged 70½ or over to transfer funds from their IRA accounts to charities in what is referred to as Qualified Charitable Distributions (QCDs). These QCDs are not taxable and where a taxpayer is also required to make required minimum distributions (RMDs), the QCDs count toward the RMD requirement. Thus, in our prior example, if the individual had transferred the $20,325 to a qualified charity in a QCD, the $20,325 would not have been taxable.

QCDs are not limited to the RMDs. For those with large IRA balances QCDs can total up $100,000 per year. Neither are QCDs limited to a single transfer in a tax year so long as the total distributed does not exceed the $100,000 annual limit.

It is important to remember that all individual’s Traditional IRAs are treated as one for purposes of determining an RMD and that all QCDs must be direct transfers by the IRA trustee to the charity.

QCD Benefits – QCDs can provide significant tax benefits. Here is how this provision, if utilized, plays out on a tax return:

- The IRA distribution is excluded from income.

- The distribution counts toward the taxpayer’s RMD for the year; and

- The distribution does NOT count as a charitable contribution deduction.

At first glance, this may not appear to provide a tax benefit. However, by excluding the distribution, a taxpayer lowers his or her adjusted gross income (AGI), which helps for other tax breaks (or punishments) that are pegged at AGI levels, such as medical expenses if itemizing deductions, passive losses, taxable Social Security income, and so on. In addition, non-itemizers essentially receive the benefit of a charitable contribution to offset the IRA distribution.

Fly In the Ointment – In the past the tax code did not permit contributions to IRAs by individuals once they reached age 70½, which coordinated with the prior age requirement to begin RMDs and the ability to make QCDs. The age restriction to contribute to IRAs has been eliminated, so now individuals may make IRA contributions at any age provided they have earned income.

Whether intentional or an oversight by Congress, the tax changes did not modify the age at which a taxpayer can begin making QCDs and left it at age 70½ – no longer in synchronization with the revised RMD age of 72.

Unfortunately that has created a situation that can be detrimental for individuals who have earned income and wish to utilize the QCD provisions and continue to contribute to an IRA after age 70½.

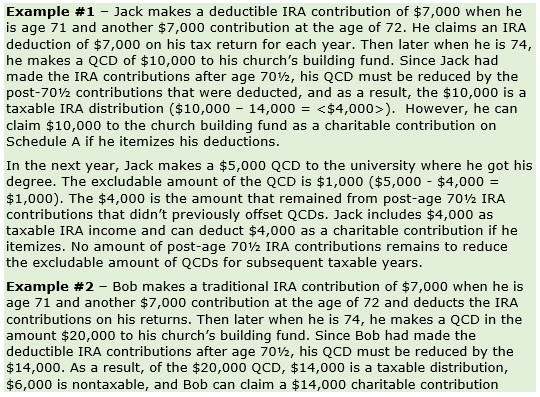

The problem being that a QCD must be reduced by the sum of IRA deductions made after age 70½ even if they are not in the same year, causing unexpected tax results for taxpayers that are not aware of this complication. This is best explained by a couple of examples.