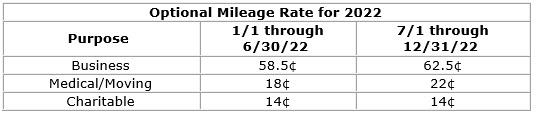

With gas prices soaring it has been expected the IRS would increase the mileage rate that business owners can deduct for vehicle use instead of keeping a record of actual expenses. Sure enough, the IRS recently announced a 4-cent increase in the optional mileage rate for the last half of 2022.

The new rate for deductible medical or moving expenses (available for active-duty members of the military) will be 22 cents for the last 6 months of 2022, also up 4 cents from the rate effective at the start of 2022. These new rates become effective July 1, 2022.

The standard mileage rate for businesses is based on a study of the fixed and variable costs of operating an automobile. The rate for medical and moving purposes is based on the variable costs as determined by the same study. The rate for using an automobile while performing services for a charitable organization is statutorily set and has been 14 cents for over 20 years.

The standard mileage rate is determined annually by the IRS using data from a study conducted by an independent contractor of vehicle-operating expenses based on the prior year’s costs. The rate includes:

- Gas,

- Oil,

- Lubrication,

- Maintenance and Repairs,

- Vehicle registration fees,

- Insurance, and

- Straight-line depreciation.

Not included in the standard rate, and deductible in addition to the optional rate, are:

- Parking,

- Tolls, and

- State and local property taxes attributable to business use.

Sales tax paid when the vehicle is purchased must be capitalized into the business basis of the vehicle, so it isn’t separately deductible.

A taxpayer may not use the business standard mileage rate for a vehicle after using any depreciation method under the Modified Accelerated Cost Recovery System (MACRS) or after claiming a Section 179 deduction for that vehicle. In addition, the business standard mileage rate cannot be used for any vehicle used for hire or for more than four vehicles used simultaneously. Taxpayers always have the option of calculating the actual costs of using their vehicle rather than using the standard mileage rates, which may produce a better result considering the skyrocketing fuel prices. Taxpayers can also switch from using the optional mileage rate in one year to actual expenses using straight line depreciation in the next year.